Atlas Insurance, 419 Ta' Xbiex Seafront, Ta' Xbiex.

Atlas Protected Cell Company facilities

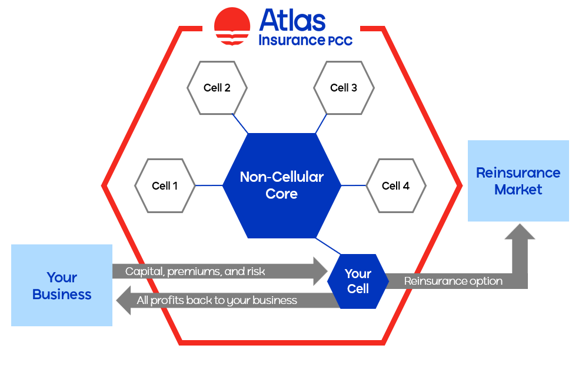

What is a Protected Cell Company?

PCCs are essentially segregated business structures in which third parties are allowed to enter as cell owners with their business ring-fenced and accounted separately. Each cell’s assets and liabilities accrue solely to the shareholders of that cell. Such cells could be used for multiple purposes such as captive risk financing tools or writing third party risks for added revenue and profit.

A feature that differentiates Maltese PCC regulation is that it presupposes individual cells have secondary recourse to PCC core capital. While absolutely protected from liabilities from the core or other cells, a cell will not have to be capitalised to the minimum EU Directive requirements for standalone insurers so long as such requirements are met by the PCC as a whole. Maltese regulations establish that once the cell has exhausted all its assets in meeting its liabilities, such cell will have perfect access (secondary recourse) to the PCC core funds. This ensures that third party policyholders or beneficiaries of a cell have the same level of protection required to be in place for other EU insurers. This is also recognised in EIOPA’s Solvency II technical specifications on the treatment of ring-fenced funds. Non-recourse provisions are allowable under regulations but solely for pure captive or reinsurance cells.